КАТЕГОРИИ:

Архитектура-(3434)Астрономия-(809)Биология-(7483)Биотехнологии-(1457)Военное дело-(14632)Высокие технологии-(1363)География-(913)Геология-(1438)Государство-(451)Демография-(1065)Дом-(47672)Журналистика и СМИ-(912)Изобретательство-(14524)Иностранные языки-(4268)Информатика-(17799)Искусство-(1338)История-(13644)Компьютеры-(11121)Косметика-(55)Кулинария-(373)Культура-(8427)Лингвистика-(374)Литература-(1642)Маркетинг-(23702)Математика-(16968)Машиностроение-(1700)Медицина-(12668)Менеджмент-(24684)Механика-(15423)Науковедение-(506)Образование-(11852)Охрана труда-(3308)Педагогика-(5571)Полиграфия-(1312)Политика-(7869)Право-(5454)Приборостроение-(1369)Программирование-(2801)Производство-(97182)Промышленность-(8706)Психология-(18388)Религия-(3217)Связь-(10668)Сельское хозяйство-(299)Социология-(6455)Спорт-(42831)Строительство-(4793)Торговля-(5050)Транспорт-(2929)Туризм-(1568)Физика-(3942)Философия-(17015)Финансы-(26596)Химия-(22929)Экология-(12095)Экономика-(9961)Электроника-(8441)Электротехника-(4623)Энергетика-(12629)Юриспруденция-(1492)Ядерная техника-(1748)

Working and Royalty Interests

|

|

|

|

Income and market approaches can be used to value working and royalty interests.

Income approach. The predominant methodology for valuing working interests and royalty interests4is an income approach, since it can be tailored to the specific property interest in question. The reserve (or engineering) report is the basis for this approach.

A PE prepares a reserve report, which contains a projection of the net cash flow the oil and gas interests are expected to generate. The PE will consider various geological and reservoir data to estimate the amount of remaining economically recoverable volumes of oil, gas, and natural gas liquids (the reserves) and the time at which such reserves will be brought to the surface and sold. The projection for each lease or well (the 8/8ths interest) is then netted to the subject interest. For valuation purposes, NYMEX oil and gas futures prices (NYMEX strip pricing), adjusted for basis differentials, are most commonly used. Lease operating costs (electricity, labor, and maintenance), taxes (severance and ad valorem), and capital expenditures for drilling additional wells are deducted. A pre-income tax cash flow projection results from this analysis. The reserve report will show a matrix of values resulting from discounting the cash flow stream at various discount rates.

For instance, the present value of the projected cash flow stream using a 10 percent discount rate is referred to as the “PV-10” value of the reserves.

The discount rate applied to the projected cash flows should properly account for the riskiness of the subject cash flow stream. The reserve report facilitates this process by categorizing the projected cash flow streams into various risk categories. The least risky category is the proved developed producing (PDP) reserves. The next categories on the risk spectrum include proved developed not producing (PDNP) and proved undeveloped (PUD) reserves. The sum of these three categories is known as “proved reserves” or “1P reserves.” Additional unproved reserve categories include probable and possible reserves.

There are three common methods for converting a reserve report to an FMV:

1. Perhaps the most accurate, but admittedly anecdotal, approach is to interview or survey investment bankers or property brokers in the oil and gas acquisition and divestiture (A&D) market regarding discount rates in effect at the valuation date. Discount rates are dependent on reserve category, location, product type (oil versus gas) and size of transaction. For example, an A&D firm might show statistics indicating that oilweighted Permian Basin PDP properties were transacting at PV-75 near the valuation date.

2. Another approach involves using data contained in an annual survey (the SPEE survey) conducted by the Society of Petroleum Evaluation Engineers.6 The SPEE survey polls about 100 experienced PEs and other experts who work in the context of A&D transactions. The section of the survey most commonly cited deals with risk adjustment factors (RAFs) used for acquisitions. The RAF isn’t a discount rate in the traditional sense, as used in the first method, but rather a “haircut” factor. While this methodology is simple, and the valuation conclusion is clear (and presumably defensible), it can be overused as a one-size-fits-all solution. For example, I interviewed an active property buyer in the Gulf of Mexico recently and found that use of the SPEE RAFs, without any further adjustment, would have significantly overvalued the offshore properties.

|

|

|

3. Another source for the discount rate is the cost of capital7 for publicly traded guideline companies. The reserve base of the guideline public companies should be sufficiently comparable to the subject properties, particularly the ratios of PDP and PUD reserves to total reserves. This approach requires a number of adjustments to reflect the public companies’ general and administrative cost structure, growth profile and marketability, which aren’t characteristics of the subject static oil and gas reserve base.

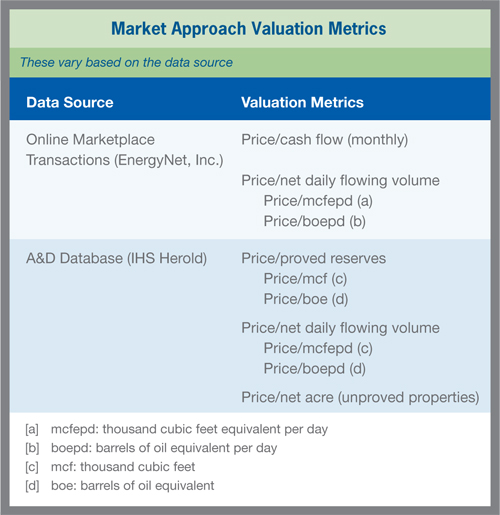

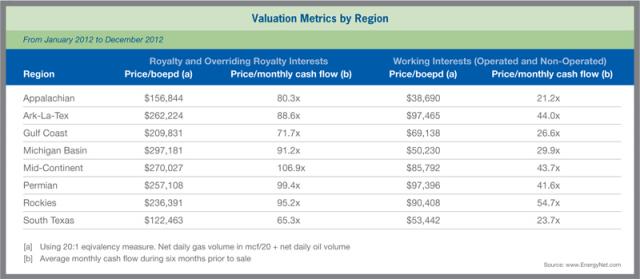

Market approach. The market approach involves applying comparable transaction metrics to the subject oil and gas property’s measures. Typical market approach valuation metrics are shown above, and sample valuation metrics by producing basin from January 2012 to December 2012 are shown on the following page. The drawback to this approach is the difficulty in finding comparable transactions. Oil and gas properties aren’t generic, and each property set can have its own unique profile. In determining whether a transaction is sufficiently comparable to the subject interest, consider whether the transactions have a similar:

· Time period (a similar oil and gas price environment)

· Basin and, if possible, same producing horizon

· Asset size

· Oil percentage of reserves

(oil versus gas-oriented transactions)

· Percentage of reserves developed/undeveloped

· Reserve life ratio (proved reserves divided by current

production rate on annual basis – the r/p ratio)

· Upside potential, a subjective factor

|

|

|

|

|

Дата добавления: 2014-12-24; Просмотров: 483; Нарушение авторских прав?; Мы поможем в написании вашей работы!