КАТЕГОРИИ:

Архитектура-(3434)Астрономия-(809)Биология-(7483)Биотехнологии-(1457)Военное дело-(14632)Высокие технологии-(1363)География-(913)Геология-(1438)Государство-(451)Демография-(1065)Дом-(47672)Журналистика и СМИ-(912)Изобретательство-(14524)Иностранные языки-(4268)Информатика-(17799)Искусство-(1338)История-(13644)Компьютеры-(11121)Косметика-(55)Кулинария-(373)Культура-(8427)Лингвистика-(374)Литература-(1642)Маркетинг-(23702)Математика-(16968)Машиностроение-(1700)Медицина-(12668)Менеджмент-(24684)Механика-(15423)Науковедение-(506)Образование-(11852)Охрана труда-(3308)Педагогика-(5571)Полиграфия-(1312)Политика-(7869)Право-(5454)Приборостроение-(1369)Программирование-(2801)Производство-(97182)Промышленность-(8706)Психология-(18388)Религия-(3217)Связь-(10668)Сельское хозяйство-(299)Социология-(6455)Спорт-(42831)Строительство-(4793)Торговля-(5050)Транспорт-(2929)Туризм-(1568)Физика-(3942)Философия-(17015)Финансы-(26596)Химия-(22929)Экология-(12095)Экономика-(9961)Электроника-(8441)Электротехника-(4623)Энергетика-(12629)Юриспруденция-(1492)Ядерная техника-(1748)

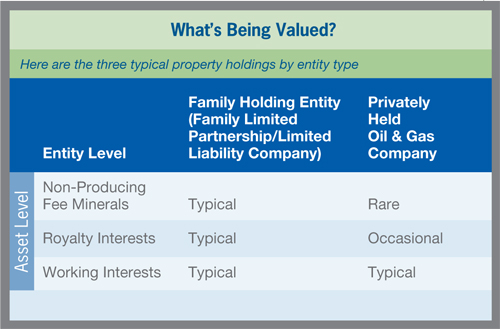

Nature of Interests

|

|

|

|

Oil and Gas Minerals: How They and Their Holding Entities Are Valued

· Alan B. Harp, Jr. · [email protected]

Spring 2013

Download PDF

Oil and natural gas valuation in an estate-planning context is becoming more important, as mineral ownership has created vast amounts of wealth in the past decade. New technologies have unlocked shale1 plays and brought older oil fields back to life. Furthermore, due to the proliferation of independent and, in many cases, private equity-backed oil and gas companies, oil and gas wealth is in the hands of more and more individuals. Estate planners advising clients who hold these assets need to know how minerals, especially non-producing minerals, and oil and gas holding entities are valued and what the Treasury regulations have to say about determining the Fair Market Value (FMV) of oil and gas interests.

Before you can understand the valuation techniques, it’s important to know the exact nature of the oil and gas interests being valued. Does the client hold primarily working interests, royalty interests, or a combination of the two? Are the interests held directly or indirectly through an entity such as a family limited partnership (FLP)? The answers to these questions dictate valuation data sources and methodology.

Here’s a simplified example, which helps to convey the definitions of, and differences among, various types of mineral interests. The most basic type of mineral interest is the fee mineral interest, representing a perpetual ownership of the mineral rights on a property, which may be separate from the land ownership. Consider a rancher who owns his land (surface rights) and underlying minerals in fee and is approached by an oil and gas company that has reason to believe oil and gas deposits may be found on (under) the ranch. The rancher may lease his minerals to the oil company in exchange for an upfront signing payment (a lease bonus) and a royalty interest in future oil and/or gas revenues. The oil company is the leasehold or working interest owner and pays all costs to drill and operate the lease. The rancher is the royalty interest owner and doesn’t bear any share of such expenses. If the rancher hasn’t leased his minerals, his ownership is called a “non-producing fee mineral interest.”2

Most of the research on oil and gas valuation focuses on working interests. Very little research has been published, and the Internal Revenue Service offers no guidance that I’m aware of, on the valuation of non-producing minerals.

|

|

|

|

|

Дата добавления: 2014-12-24; Просмотров: 430; Нарушение авторских прав?; Мы поможем в написании вашей работы!