КАТЕГОРИИ:

Архитектура-(3434)Астрономия-(809)Биология-(7483)Биотехнологии-(1457)Военное дело-(14632)Высокие технологии-(1363)География-(913)Геология-(1438)Государство-(451)Демография-(1065)Дом-(47672)Журналистика и СМИ-(912)Изобретательство-(14524)Иностранные языки-(4268)Информатика-(17799)Искусство-(1338)История-(13644)Компьютеры-(11121)Косметика-(55)Кулинария-(373)Культура-(8427)Лингвистика-(374)Литература-(1642)Маркетинг-(23702)Математика-(16968)Машиностроение-(1700)Медицина-(12668)Менеджмент-(24684)Механика-(15423)Науковедение-(506)Образование-(11852)Охрана труда-(3308)Педагогика-(5571)Полиграфия-(1312)Политика-(7869)Право-(5454)Приборостроение-(1369)Программирование-(2801)Производство-(97182)Промышленность-(8706)Психология-(18388)Религия-(3217)Связь-(10668)Сельское хозяйство-(299)Социология-(6455)Спорт-(42831)Строительство-(4793)Торговля-(5050)Транспорт-(2929)Туризм-(1568)Физика-(3942)Философия-(17015)Финансы-(26596)Химия-(22929)Экология-(12095)Экономика-(9961)Электроника-(8441)Электротехника-(4623)Энергетика-(12629)Юриспруденция-(1492)Ядерная техника-(1748)

Diversification

|

|

|

|

Portfolio Risk and the Importance of Covariance

Although the portfolio expected return is a straightforward, weighted average of returns on the individual securities, the portfolio standard deviation is not the simple, weighted average of individual security standard deviations. To take a weighted average of individual security standard deviations would be to ignore the relationship, or covariance, between the returns on securities. This covariance, however, does not affect the portfolio's expected return.

Covariance is a statistical measure of the degree to which two variables (e.g., securities' returns) move together. Positive covariance shows that, on average, the two variables move together. Negative covariance suggests that, on average, the two variables move in opposite directions. Zero covariance means that the two variables show no tendency to vary together in either a positive or negative linear fashion. Covariance between security returns complicates our calculation of portfolio standard deviation. Still, this dark cloud of mathematical complexity contains a silver lining—covariance between securities provides for the possibility of eliminating some risk without reducing potential return.

The concept of diversification makes such common sense that our language even contains everyday expressions that exhort us to diversify ("Don't put all your eggs in one basket.")- The idea is to spread your risk across a number of assets or investments. While pointing us in the right direction, this is a rather naive approach to diversification. It would seem to imply that investing $10,000 evenly across 10 different securities makes you more diversified than the same amount of money invested evenly across 5 securities. The catch is that naive diversification ignores the covariance (or correlation) between security returns. The portfolio containing 10 securities could represent stocks from only one industry and have returns that are highly correlated. The 5-stock portfolio might represent various industries whose security returns might show low correlation and, hence, low portfolio return variability.

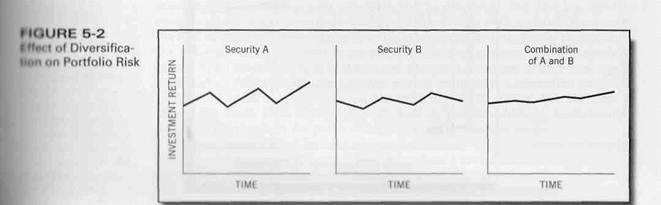

Meaningful diversification, combining securities in a way that will reduce risk, is illustrated in Figure1. Here the returns over time for security A are cyclical in that they move with the economy in general. Returns for security B, however, are mildly countercyclical. Thus, the returns for these two securities are negatively correlated. Equal amounts invested in both securities will reduce the dispersion of return, on the portfolio of investments. This is because some of each individual security's variability is offsetting (нейтрализующий). Benefits of diversification, in the form of risk reduction, occur as long as the securities are not perfectly, positively correlated.

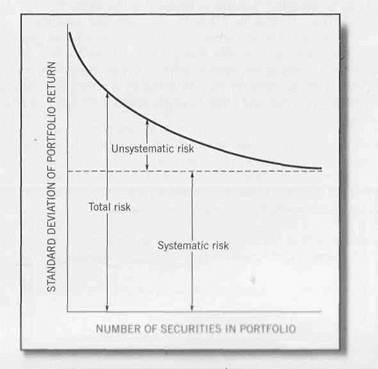

Research studies have looked at what happens to portfolio risk as randomly selected stocks are combined to form equally weighted portfolios, When we begin with a single stock, the risk of the portfolio is the standard deviation of that one stock. As the number of randomly selected stocks held in the portfolio is increased, the total risk of the portfolio is reduced. Such a reduction is at a decreasing rate, how ever. Thus, a substantial proportion of the portfolio risk can be eliminated with a relatively moderate amount of diversification, say, 15 to 20 randomly selected stocks in equal-dollar amounts. Conceptually, this is illustrated in Figure 2.

|

|

|

|

|

|

Дата добавления: 2014-01-11; Просмотров: 573; Нарушение авторских прав?; Мы поможем в написании вашей работы!