КАТЕГОРИИ:

Архитектура-(3434)Астрономия-(809)Биология-(7483)Биотехнологии-(1457)Военное дело-(14632)Высокие технологии-(1363)География-(913)Геология-(1438)Государство-(451)Демография-(1065)Дом-(47672)Журналистика и СМИ-(912)Изобретательство-(14524)Иностранные языки-(4268)Информатика-(17799)Искусство-(1338)История-(13644)Компьютеры-(11121)Косметика-(55)Кулинария-(373)Культура-(8427)Лингвистика-(374)Литература-(1642)Маркетинг-(23702)Математика-(16968)Машиностроение-(1700)Медицина-(12668)Менеджмент-(24684)Механика-(15423)Науковедение-(506)Образование-(11852)Охрана труда-(3308)Педагогика-(5571)Полиграфия-(1312)Политика-(7869)Право-(5454)Приборостроение-(1369)Программирование-(2801)Производство-(97182)Промышленность-(8706)Психология-(18388)Религия-(3217)Связь-(10668)Сельское хозяйство-(299)Социология-(6455)Спорт-(42831)Строительство-(4793)Торговля-(5050)Транспорт-(2929)Туризм-(1568)Физика-(3942)Философия-(17015)Финансы-(26596)Химия-(22929)Экология-(12095)Экономика-(9961)Электроника-(8441)Электротехника-(4623)Энергетика-(12629)Юриспруденция-(1492)Ядерная техника-(1748)

Outline. Lecture 1. Management Accounting: Definition, Development, Aim and Tasks

|

|

|

|

Lecture 1. Management Accounting: Definition, Development, Aim and Tasks

Management Accounting

Частина 2

Відповідальний за випуск Ю.М.Лопаткін Редактор Н.З.Клочко

Комп’ютерне верстання О.В.Лисенка

Підп. до друку 12.07.2010, поз 156.

Формат 60x84/8. Ум. друк. арк. 28,83. Обл.-вид. арк. 22,37. Тираж 100 пр. Зам. № 1168.

Собівартість вид. 42 грн 54 к.

Видавець і виготовлювач Сумський державний університет,

вул. Римського-Корсакова, 2, м. Суми, 40007

Свідоцтво суб'єкта видавничої справи ДК №3062 від 17.12.2007.

1. The Notion of Management Accounting. The Aim and Tasks of Management Accounting.

2. The Development of Management Accounting. Management Accounting vs. Financial Accounting.

1. Management Accounting. Why necessary?

The notion and the process of Management Accounting has not been developed yet at Ukrainian enterprises as the complex system of collecting, analyzing, interpreting and providing the information necessary for the managers who make quick, tactic and strategic decisions.

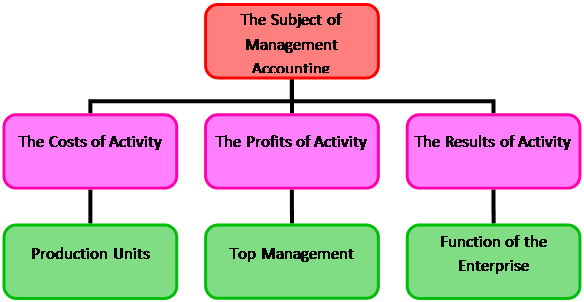

The essence of Management Accounting, its application can be defined as a ‘production’ of information to make management effective.

There are several reasons why Management Accounting has become necessary to introduce at the enterprises:

- Introduction of various forms of ownership leads to different groups and levels of users of management information;

- Competition at internal and external markets of Ukrainian products and as a result a strong need of being informed about their conjuncture;

- Integration of Ukrainian economy into the international one leads to the changes in accounting practice.

Therefore there are several requirements to a new-developed system of accounting as for the amount and contents of information that is given:

- Timeliness - the given data should outstrip any decision, that’ is why the procedure and frequency of the information provided should match the character and frequency of management decisions.

- Differentiation- the information provided must be sufficient enough to assist the manager to make an appropriate decision.

- Simplicity – the information should be easy understandable by any manager: senior or subordinate.

- Compact Size – reports should be abridged but not too much to let the manager control and check not only final results but also current indices.

- Variability – the information should present the option for making the decision.

The system of Management Accounting goes beyond the accounting and includes the elements of planning, control, analysis, evaluation which causes disagreements among its researchers.

The main task of Management Accounting is the provision of unbiased information necessary for decision-making by certain managers of the enterprise.

2. How did the process of Management Accounting develop?

Having appeared as cost accounting, management accounting has several stages of development:

· Analytical (before WWII)

· Marginal (by 1975)

· Strategic (till present)

Management Accounting is an integrated system of various economic disciplines, its method includes:

- The elements of accounting (accounts and double-entry bookkeeping, inventory and documentation, evaluation and calculation)

- The elements of statistics (index method)

- The method of economic analysis (factor analysis)

- Mathematic methods (correlation, linear programming, least squares procedure)

Management Accounting is a part of Accounting in general and it is closely related to Financial Accounting in its principles:

· The continuity of activity of enterprise

· A single money measure

· Completeness and analyticity of information

· Frequency (periodicity, cyclicity)

Still there are purely Management Accounting principles:

- The principle of evaluation of the activity in the structural units of enterprise – defining the tendencies and perspectives of each unit in profit-making from the production to sales of products.

- The principle of integration – a single data statement in the initial documents or production calculations and their overall use in various management activities.

- The principle of budget method of management – budgeting of production, sales and financing of structural units and enterprise as a whole.

- The principle of dependence – the costs dependent on future choice are related to different alternative decisions.

- The principle of reasoning – the costs incurred in the production of certain product can be related to the unit cost of this very product.

The functions of Management Accounting are:

- Information

- Communication

- Control

- Forecasting

There are several differentiations in the relation of financial accounting and management accounting.

- Necessity of accounting

- The aim of accounting

- The users of information

- Measures

- The objects of accounting

- The frequency of accounts

- The accuracy of accounts

- The time aspect

- The degree of information transparency

- Direction

There are three approaches in accounts management of management accounting in the system of universal accounting: general, autonomous (two-row) and integrated (single-row).

General system is used by small enterprises of service industry, trade, manufacturing not taking into account calculation of unit cost of product. It is based on periodic stock taking, differentiated cost accounting according to elements (accounts of class 8) and revenues of their classes (accounts of class 7) and financial result in special account (account 79).

Integrated system is used by large enterprises based on cost accounting of “Production”, “General Production Costs”, “Sales Costs” which correspond to financial accounting and which are accounted for considering different groups of costs, their sources, types of products etc.

Autonomous (two-row) system means keeping records of financial and management accounting which do not correspond. Financial accounting records costs of the elements, revenues of their types, debtors and creditors, general financial result. Management accounting using the same information records stock taking, production and sales costs (with necessary analytic details), unit cost of the product financial result from sales of the product.

The relation of financial and management accounting is shown in CONTROL ACCOUNTS. These accounts (Control Account of Production Accounting, Control Account of Financial Accounting) have an opposite structure. The balance in Control Account of Production Accounting characterizes the general value of stocks which is given in production accounts and is considered a commercial secret.

Home Assignment: Find and review the definition of Financial Accounting!!!

|

|

|

|

Дата добавления: 2014-01-11; Просмотров: 725; Нарушение авторских прав?; Мы поможем в написании вашей работы!